Settling Abroad Money / Late-Start Retirement

Quick answer: If you feel behind, start with visible numbers: income floor, fixed costs, healthcare, documents, bridge income, trial stay, decision date, and return-home reserve.

A late-start retirement plan should not begin with shame. It should begin with a short list of things that can be checked, priced, tested, or scheduled.

The useful question is not whether the plan is perfect today. The useful question is which gaps have to be made visible before a long stay abroad becomes financially calm instead of fragile.

This guide is a plain-English planning framework. It is not investment, tax, legal, benefits, insurance, Social Security, Medicare, or retirement advice. Verify your income, taxes, healthcare, benefits, insurance, and legal situation with official sources and qualified professionals.

Being late is not the same as being stuck. Visible gaps can be worked.

Make the gap visible first

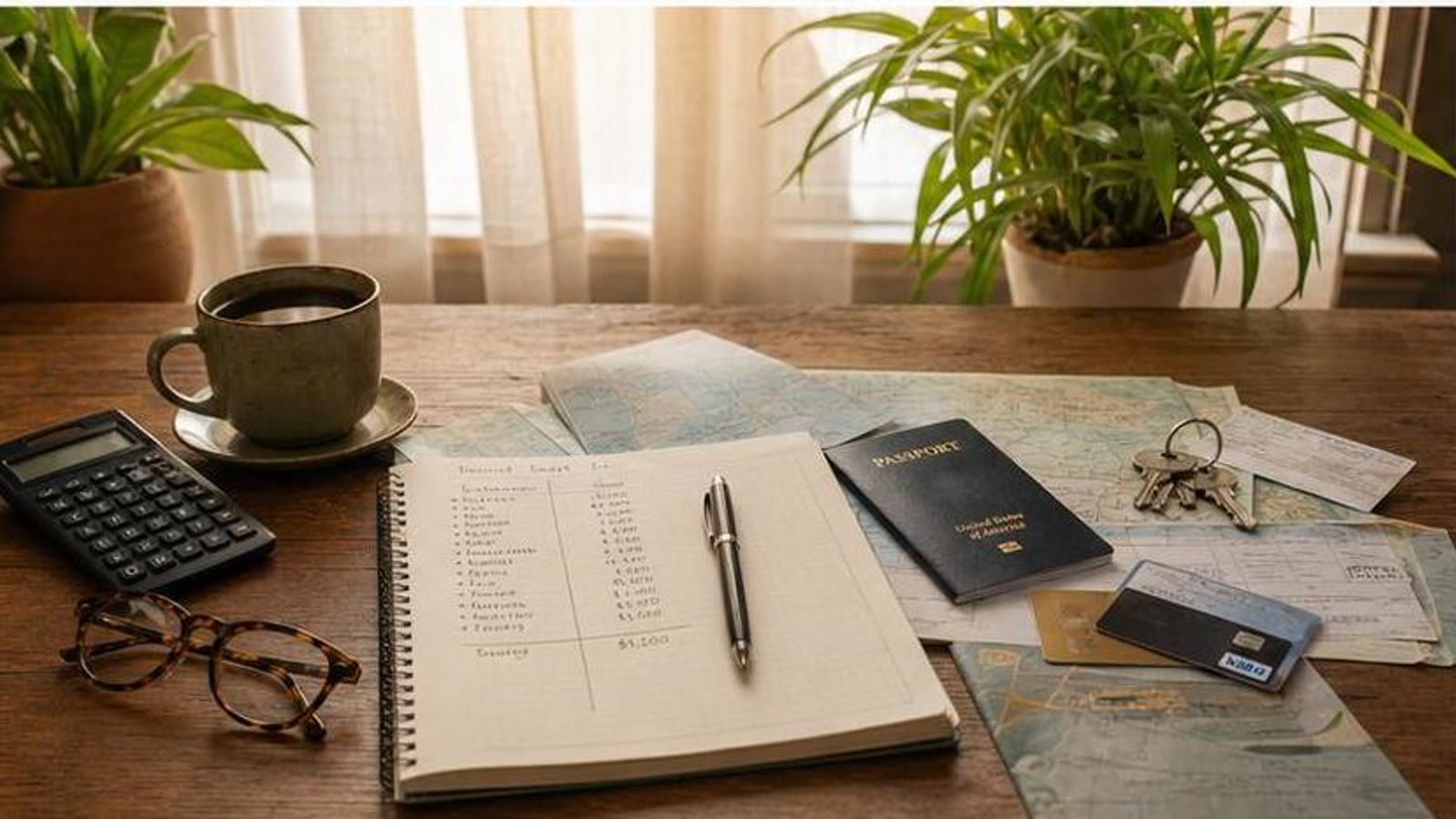

Write down dependable monthly income, likely Social Security timing, pension income, savings withdrawals, debt, insurance, housing costs, tax filing needs, family obligations, and the cash reserve you want before leaving.

Use net monthly numbers where possible. If a number is only a guess, label it as a guess. If a number depends on a future tenant, job, sale, or benefit decision, keep it separate from the dependable income floor.

Cut fixed costs before choosing a country

A cheaper destination can help, but it should not be asked to rescue a U.S. budget that still has too many fixed costs. Debt, storage, unused cars, insurance, subscriptions, and housing decisions deserve attention before the move is urgent.

Cutting a recurring bill by a few hundred dollars can matter more than finding a slightly cheaper apartment overseas. It improves every destination option, including the option to come home.

Solve healthcare and document access early

Healthcare planning needs more than a hopeful monthly number. List prescriptions, doctors, records, insurance, Medicare timing, travel coverage, cash-pay backup, emergency contacts, and the route home if care becomes complicated.

Do the same with documents. Passport, insurance cards, tax files, bank contacts, medication lists, housing paperwork, and emergency instructions should be stored securely and reachable from more than one device.

Turn the trial stay into a decision tool

A trial stay should measure daily life, not just vacation appeal. Track housing, groceries, transportation, healthcare access, internet, weather, language friction, loneliness, errands, sleep, and how often you still need to fly back to the U.S.

Set success criteria before you go. If the stay is meant to test a $2,500 monthly life, do not judge it by a two-week vacation budget.

A late-start retirement checklist

- Income floor: dependable monthly income, flexible income, and the gap that remains.

- Fixed costs: debts, insurance, storage, cars, subscriptions, taxes, and housing obligations.

- Healthcare: prescriptions, records, coverage, Medicare timing, local care, and return-home backup.

- Documents: secure digital copies, emergency contacts, tax files, bank contacts, and access from a second device.

- Bridge: part-time work, delayed benefits, rental income, downsizing, or another realistic gap-covering plan.

- Trial stay: one practical base, a real monthly budget, success criteria, and a decision date.

Mistakes to avoid

- Letting embarrassment keep the numbers hidden.

- Researching destinations while ignoring fixed costs that follow you.

- Moving permanently before one serious trial stay.

- Waiting until departure to organize healthcare records and documents.

- Using the cheapest possible month as the retirement plan.

Pick the one checklist item you have been avoiding and turn it into a number, document, phone call, or date this week.

Bottom line

A late-start retirement checklist is not a confession that you are behind. It is a way to stop carrying the whole plan in your head.

Once the income floor, fixed costs, healthcare, documents, bridge, trial stay, and return-home reserve are visible, the next step becomes less emotional and much easier to test.

Sources

Use these as starting points for official rules and program details. For personal tax, benefits, investment, insurance, Medicare, Social Security, or legal decisions, verify your situation directly with the agency or a qualified professional.